Hyperinflation: Is there a right way to prepare for it?

24 May 2022

Ever heard your folks say something like: “In our time, I can buy much with $1.” In a way, it’s a rant about how times and spending changed, but it is a reality we ought to live with.

Even you can personally attest to how your $2-bill could buy you a decent chicken rice meal a couple of years ago, whereas today, you can expect to pay $5 or more for the same serving size.

This is called inflation. The value of our money usually decreases.

Inflation could be healthy for an economy… unless the rate becomes insanely high within a period of time. Such is what we call “hyperinflation.”

Last year, the United States saw a 6% inflation rate, the highest since 2011 (3.5%). This annual inflation rate was a huge jump from the previous years, 1.2% in 2020 and 1.9% in 2019.

Understandably, the global population fears the possibility of hyperinflation, given this alarming inflation rate in the US.

What is hyperinflation

In simple terms, hyperinflation is out-of-control inflation. It happens when the price of goods and services uncontrollably rises over time. Economists set a benchmark percentage for this increase in prices – at an annual rate of 1,000% or more.

Let’s paint a picture of when inflation is considered healthy in comparison to it becoming a “hyperinflation.”

A low level of inflation, 1 to 2% for instance, makes the economy alive. Prices that increase slowly over time will encourage consumers and businesses to spend their money.

But when hyperinflation happens, a sack of rice could double in price every single day. And no, this didn’t come straight from fiction. It’s what happened in Hungary after World War II and in Venezuela in 2016.

Some believe hyperinflation is likely to happen given current circumstances, but some experts do not think so.

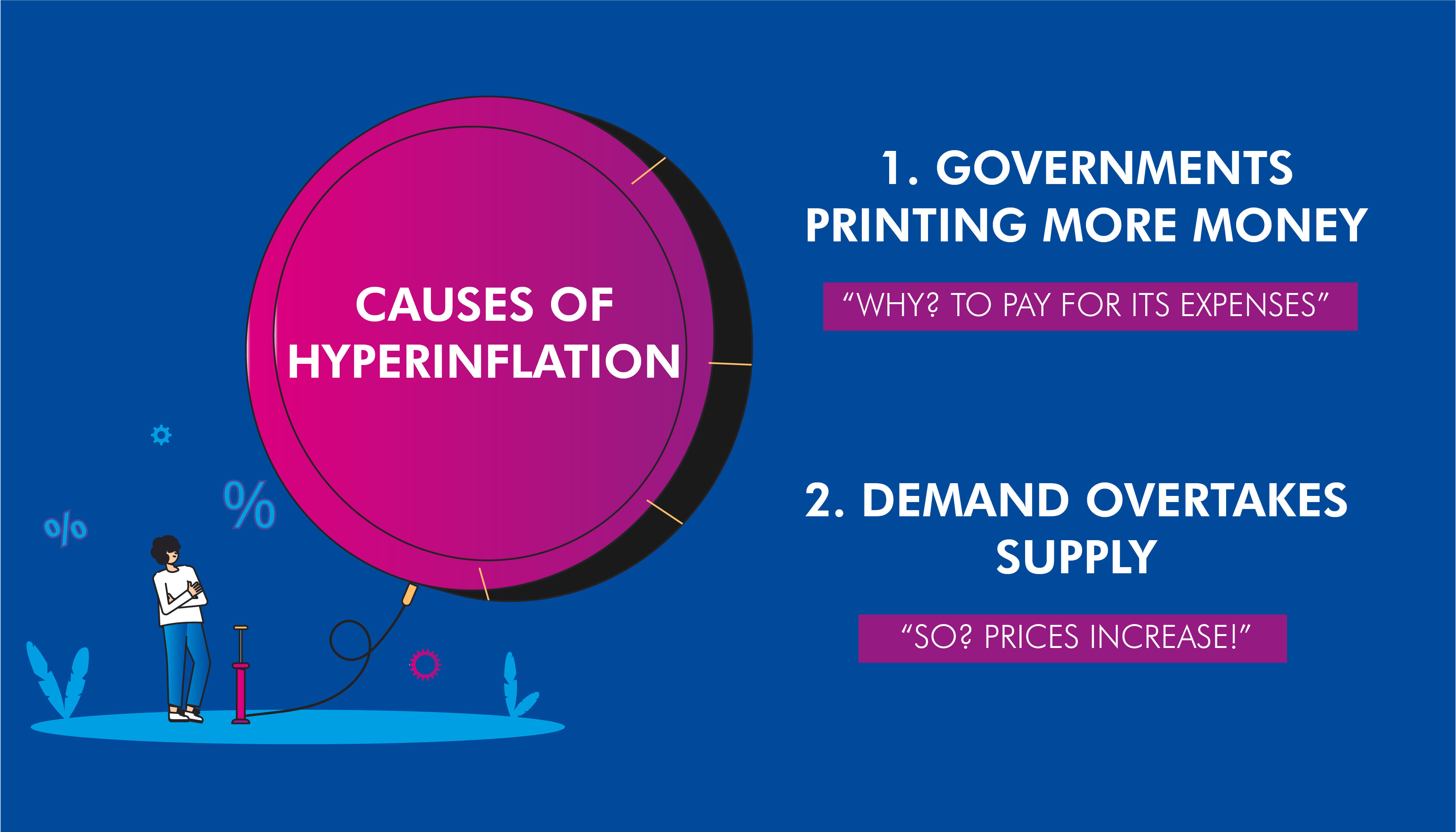

What causes hyperinflation

Hyperinflation occurs when either of two scenarios happens: when the money supply increases without economic growth to support it or when the demand outstrips the supply.

Why would the money supply increase when economic growth is absent? This happens when governments print more money to fund their expenses. They would print money in response to a crisis or several crises they are facing.

For example, if there’s a war and the global supply chains are impacted, a government can opt to just print money to pay its spending instead of using typical taxation methods.

Other triggers for such a situation include a social uprising, an insane debt in foreign currency, or a supply shock.

At first glance, you might not see this posing any problem. The government gets more money… so what’s the problem? The issue comes with consumers and businesses realising that the value of their money will decrease even more – basically, the concept of inflation.

Demand-pull inflation (the case when demand outstrips supply), on the other hand, is quite self-explanatory. When the economy is rapidly growing and there is increased consumer spending, this could happen, thereby, sending the prices higher, too.

Having explained these two scenarios, we hope you now understand why the fear of upcoming hyperinflation is warranted.

First, the global economy suffered during the pandemic. We saw supply chains halted, movements disrupted, and businesses liquidated during the past couple of years. Then came the uncertainty and further volatility due to the Russia-Ukraine war.

In the US alone, food prices increased by 9.2% in the past year whereas energy costs increased by 33.9%. But this situation isn’t an isolated case. Countries around the world, including in Asia, are likewise feeling the effect of the crises. Banks have also announced hikes in their interest rates to combat the rising inflation.

As a retail investor, how do you prepare for looming hyperinflation?

How to prepare for hyperinflation

Don’t ever say hyperinflation might not happen anytime soon, because we don’t have a crystal ball to predict that. And if it doesn’t happen, well it’s always better to be prepared, isn’t it?

So how you do protect your wealth? Should you start investing? Should you continue to invest or is it time to withdraw all your investments?

By not investing your money, you’re not preparing for hyperinflation. We invest because we want to outrun inflation rates, so why withdraw your investments when the value of your money risk being greatly reduced?

Why not invest it instead and keep it where it can grow?

You have four options for investment before hyperinflation hits: stocks, real estate, bonds, and commodities.

Real estate (including real estate investment trusts or REITs) and commodities might be two of your best options when you want a hedge against inflation. These non-cash assets won’t see your money grow in the shortest time, but they are investment types that can protect your hard-earned money.

Another option is to invest in fixed-income assets, including bonds and especially short-term or floating rate bonds. This is because this type of bond is less susceptible to changes in interest rates.

Stock investing can also be an option. But choose carefully. You wouldn’t want a stock that just looks good outside but is frail inside.

Invest in stocks that are “safer” – meaning those that have good fundamentals, those that you’re confident would still grow and make money in the next 5 to 10 years. Look for a stock whose underlying business has a strong economic moat.

This way, you won’t need to panic every time the market turns red or there are reports of a bearish market looming.

Hyperinflation will erode our hard-earned money. Make sure you’re prepared for it. Don’t worry, we’ll help you out. Come to our FREE investment masterclass as we teach you how to pick the best investments at a turbulent time like today.

DISCLAIMER

This article and its contents are provided for information purposes only and do not constitute a recommendation to purchase or sell securities of any of the companies or investments herein described. It is not intended to amount to financial advice on which you should rely.

No representations, warranties, or guarantees, whether expressed or implied, made to the contents in the article is accurate, complete, or up-to-date. Past performance is not indicative nor a guarantee of future returns.

We, 8VI Global Pte Ltd, disclaim any responsibility for any liability, loss, or risk or otherwise, which is incurred as a consequence, directly or indirectly, from the use and application of any of the contents of the article.