Why should you use a retirement calculator?

13 Dec 2021

Procrastination costs us our dreams.

As we repeatedly press “snooze” on our alarm clocks, we lose the chance to do a 30-minute morning stroll. As we postpone sending a pitch, we lose the opportunity to be considered for a huge project.

Every “I promise to plan my retirement tomorrow” is a missed chance to get a concrete strategy to realising our travel bucket list for when we’re 50.

So go ahead, set aside a couple of hours to lay down your retirement plan. No more procrastinating about a chapter we’re all going to start sooner rather than later.

One tool you can leverage in retirement planning is the retirement calculator. It’s an easy-to-use tool that tells you how much you need to save from today onwards for you to achieve your desired lifestyle in your sunset years.

If you aren’t the same as the majority and actually started saving for your retirement, then that’s great news, you can use a retirement calculator to determine whether what you’re currently saving is enough for what you aspire to have two or three decades from today.

Retirement calculators abound

What’s amazing about the world we live in today is the availability of a wide range of choices at our disposal. Retirement calculators are a pretty common tool offered by banks, insurance companies, and investment firms. You can just search for one that has features that you like and use it. Or you can test out different retirement calculators to compare and contrast, too.

Retirement calculators have the same purpose, but they vary in complexity. Some calculators require you to input your social security savings, salary increments per year, and risk profile. Some calculators are so simple they just ask you for your desired retirement income and your age.

If you’re a Singapore Citizen or PR, you can test out the CPF Board’s free retirement calculator where you’ll see a detailed summary of what your retirement strategy should constitute.

If you’d rather use a simple retirement calculator (and don’t want to input your CPF account details), check out VI App – it’s essentially a stock analysis tool but it has a simple-to-use and free retirement calculator you can use when you register for an account.

How retirement calculators work

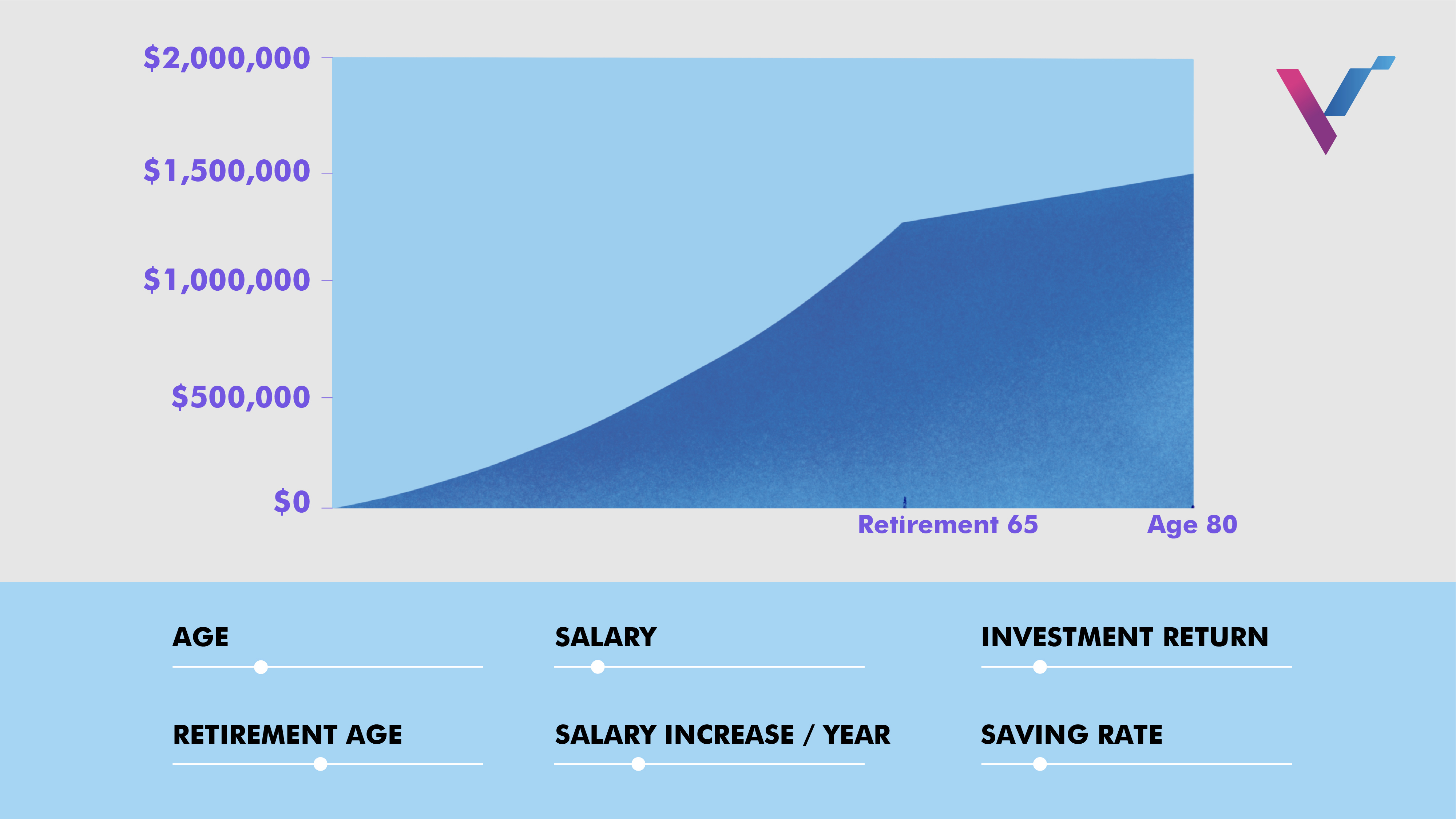

The beauty of using a retirement calculator is everything is easy. You just need to input or choose the required details, and the calculator will automatically furnish you with the numbers.

These calculators can do this because they are developed to use financial formulas that compute the figures you input. With these formulas are assumptions on percentages such as investment growth rate and inflation rate that would affect the numbers. From there, the tool will recommend what your next steps should be.

Take for instance a 25-year-old who is done procrastinating and is now taking the first step to planning her retirement. Perhaps she doesn’t have huge savings yet, but if she plans to save 30% of her monthly income for retirement, the calculator will be able to tell her if 30% is sufficient to allow her to retire at, say 50 at $2,500 retirement income per month.

A retirement calculator typically has the following components:

- Your current age

- Your desired retirement age

- Your expected retirement period

- Your current income per month

- Your desired retirement income per month

- Your current savings

- The amount you’re willing to set aside for retirement

Some, as mentioned above, have more items to tick, but you catch the drift.

What retirement calculators cannot tell you

Retirement calculators are powerful tools for retirement planning, we all agree on that. But these tools have limitations, too.

You can’t expect to have your retirement plan all sorted out after using a retirement calculator. For one, these calculators do not cover every factor that could impact your retirement.

To illustrate, most, if not all, retirement calculators don’t include taxes in their formulas. Taxes should be considered in your planning as they affect your current expenses and your retirement expenses as well.

Likewise, emergencies happen and we won’t know when we need to spend for a major expense in the years before retiring, and this could impact our plan. We also don’t have an idea of whether the retirement income we wish to have will be enough to cover our lifestyle, considering that the sunset years could mean more medical and caregiving expenses.

Hence, checking how much you should save for retirement using a retirement calculator is just one step in planning. What comes next are equally important.

If your calculations yielded a conclusion that your current income percentage allocation to your retirement is not enough to allow you to retire at 55, you can’t just raise a white flag and just give up on retiring early. Your next question should be: What can I do to achieve my goal?

Some solutions to your question include increasing your savings per month, changing your lifestyle, and investing your money.

Take some time to think about it. Ask a friend. Look for opportunities. And most importantly, don’t procrastinate. Once you’ve figured out your retirement plan, trust us, you can sleep peacefully at night and hit the “snooze” button without feeling guilty.

See how retirement calculators work and how you can create additional passive income for your sunset years. Register for a free seat in our investment bootcamp.

DISCLAIMER

This article and its contents are provided for information purposes only and do not constitute a recommendation to purchase or sell securities of any of the companies or investments herein described. It is not intended to amount to financial advice on which you should rely.

No representations, warranties, or guarantees, whether expressed or implied, made to the contents in the article is accurate, complete, or up-to-date. Past performance is not indicative nor a guarantee of future returns.

We, 8VI Global Pte Ltd, disclaim any responsibility for any liability, loss, or risk or otherwise, which is incurred as a consequence, directly or indirectly, from the use and application of any of the contents of the article.