Dollar-Cost Averaging: Rewards, Drawbacks, Tips

29 Apr 2022

Doing the same thing every time may not be everyone’s cup of tea but we can’t deny that it’s definitely an easy task. Now imagine applying this concept to stock investing.

That’s what we call the dollar-cost averaging (DCA) strategy.

You might have heard the term before, but if you’re curious about how it’s actually done and whether investors like you would really profit from this strategy, then keep reading.

Dollar-cost averaging

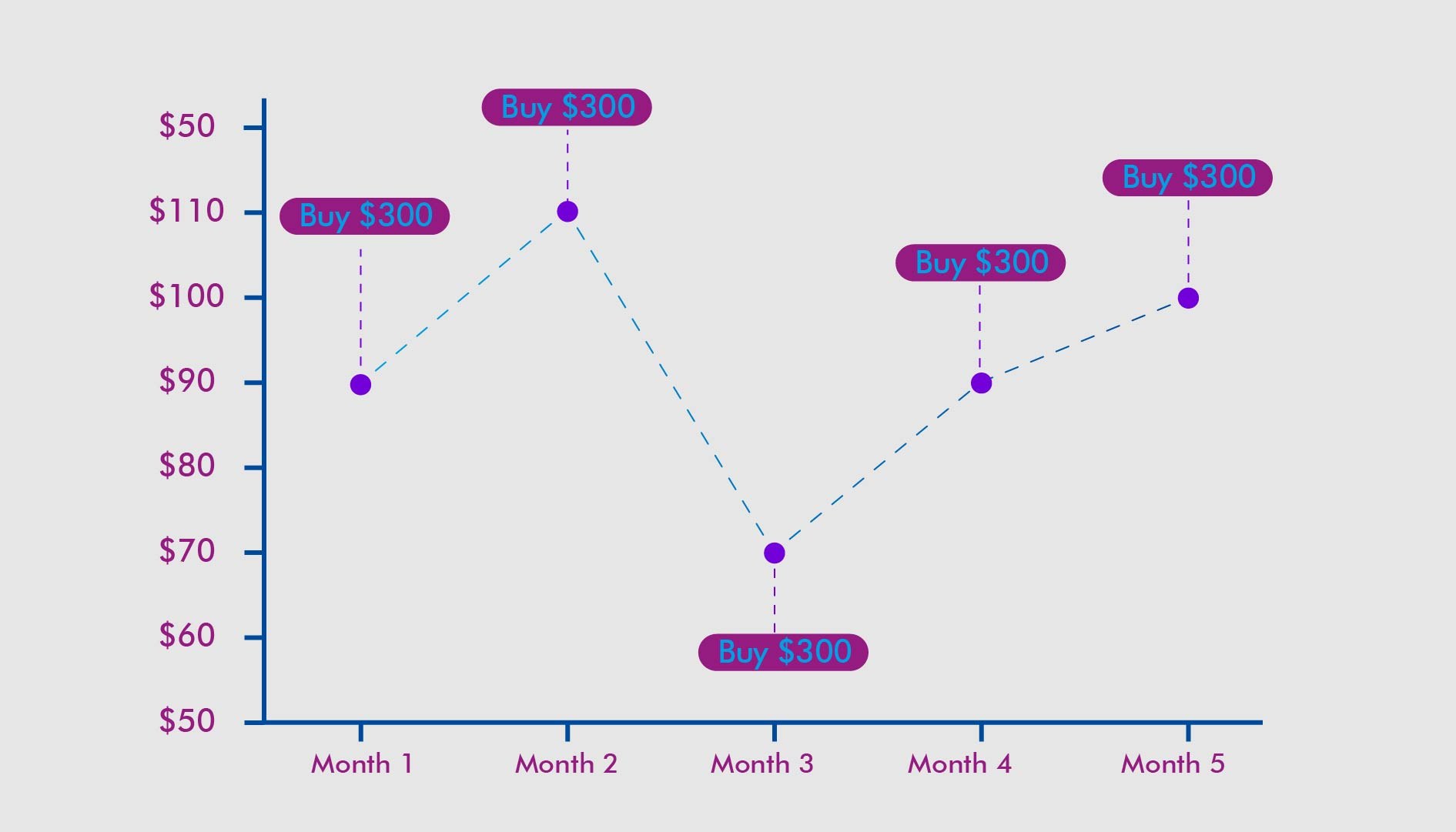

When you do dollar-cost averaging, you’re essentially investing the same amount of money in a stock, say Roblox (NYSE: RBLX), periodically.

For example, if you set aside $1000 last year, 2021, to invest into Roblox, and then $1000 this year, $1000 next year, and so on, that’s doing dollar-cost averaging.

Or if you, for instance, set aside $300 monthly to invest in another stock, say Starbucks (Nasdaq: SBUX), that’s doing dollar-cost averaging as well.

Another example is when you invest in an exchange-traded fund, like SPY ETF, with $500 per month or per quarter.

Basically, you’re investing an equal amount on the same asset at regular intervals... and yes, regardless of whether the share price for that period went up or down.

When the price goes up, you can only buy a small number of shares, depending on the amount you set aside. When the price drops, you can buy more shares.

How investors get rewarded

Dollar-cost averaging is quite easy to do. You can easily track how much you’re investing. But do investors really get rewarded for using this strategy, given how easy it is?

The short answer is YES, they do.

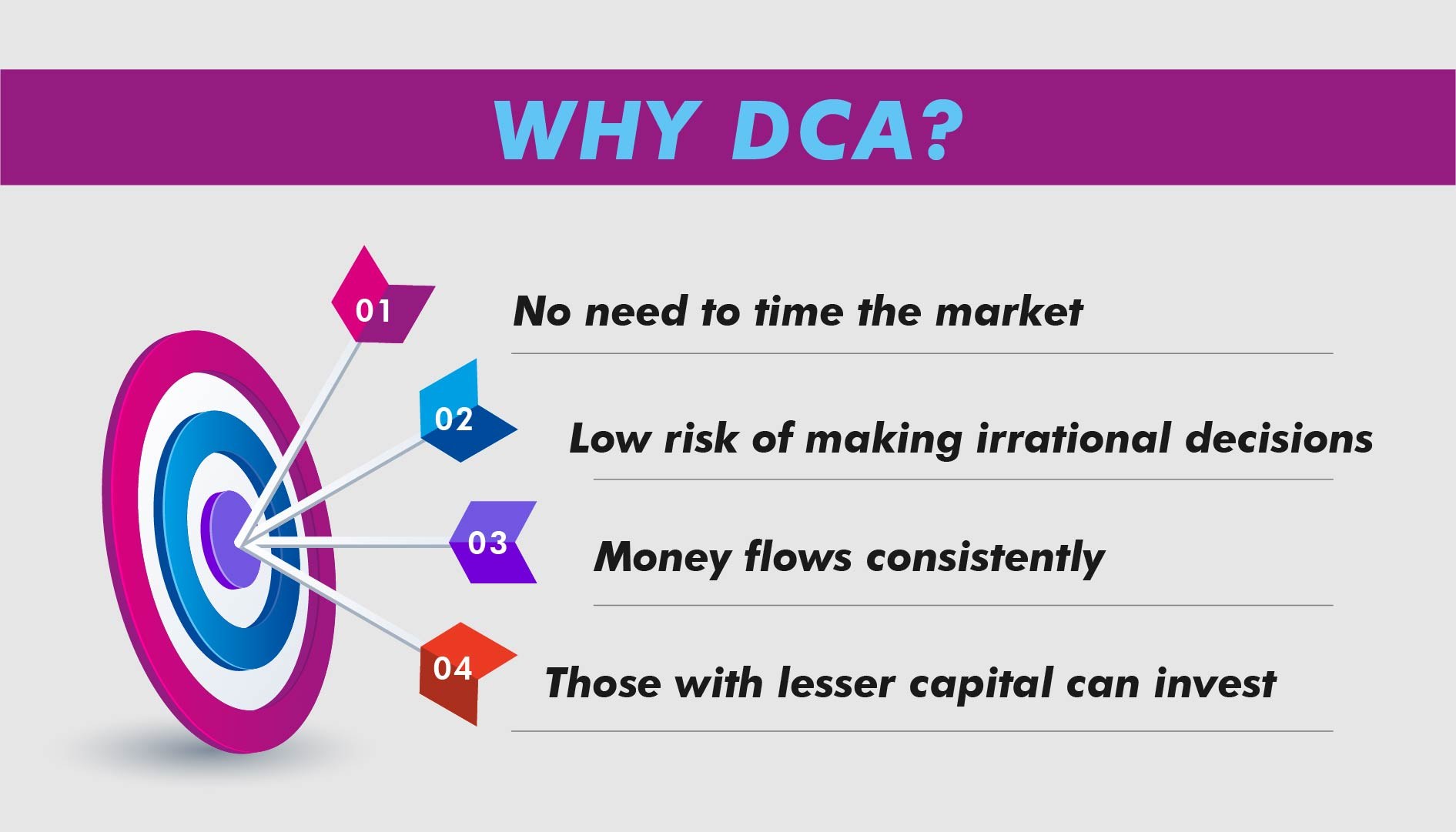

Here are the advantages of dollar-cost averaging for investors:

1. No more timing the market

Timing the market is difficult, if not impossible.

With dollar-cost averaging, as you are regularly investing in a stock, you won’t really care much about when the best prices will come... ‘cause, sorry to burst your bubble, there’s absolutely no way of knowing it anyway. We aren’t trained to be fortune tellers in the stock market, are we?

Likewise, investors who apply dollar-cost averaging want to leverage long-term investing. They usually stay invested even during bearish markets, hoping to acquire great buys and see rewards once the market goes bullish again.

2. Emotions are better managed

With the expectation of timing the market comes the risk of illogical decisions stemming from harmful emotions, like greed, fear, and envy.

We all know this. We tend to get emotional and all panicky when the market seems to sway against our objectives. Hence, panic buying and panic-selling cause investors to lose money rather than grow it.

But with dollar-cost averaging, the focus is on the price you set aside for the investment, regardless of the market movement. Investors then can avoid temptations arising from greed or fear.

3. Money works consistently

Investing in a stock with equal amounts spread over regular intervals also translates into having your money work consistently for you.

This is because the stock market, historically, goes up. Hence, dollar-cost averaging helps you make profits over the long term when the prices rise and as your investments also grow. Plus, you’re paying a lower average price when you make multiple purchases.

4. Limited capital is not an issue

Dollar-cost averaging is best for starting investors who usually have lesser capital. Your small amount of money can purchase stocks and allow you enough time to save money for future investments. Thus, there’s no need to secure a really high capital before buying your very first stock.

Likewise, as mentioned above, bear markets provide opportunities for those with little capital to buy undervalued stocks and make profits in the long term.

But is there any downside?

Dollar-cost averaging is only one of several strategies you can adopt. So, of course, there are criticisms against its use as well as doubts about the returns it generates. These are warranted.

One obvious drawback of dollar-cost averaging is the high cost it entails. Since you’ll be buying stocks at regular intervals, perhaps monthly or quarterly, the transaction fees need to be paid. And these could balloon, especially when your broker implements really high fees.

Another downside is the missed chance to profit handsomely vis-a-vis the amount you invested. Critics believe that investing in lump sums or huge amounts on a stock has a greater chance of gaining higher returns.

To illustrate, if you invest $10,000 in a stock and the share price jumps after a couple of months, you’re $10,000 is sure to make good money. Compare it with investing in the same stock with only $500 monthly ($1000 total investment), the results would understandably be more disappointing.

Yet, it’s always up to you to manage your expectations with respect to these downsides. For one, transaction fees are non-negotiable. Second, the example above is for when the market turns bullish after a few months of investing... how about when it turns bearish?

We aren’t in any way telling you that dollar-cost averaging is the way to go. We want you to gauge both its advantages and disadvantages so you can decide for yourself.

A couple of tips to note

Should you decide to explore this strategy, here are some tips for you.

1. Do your due diligence in choosing stocks

Your money will be invested in a stock for years. It’s only necessary to find one you’re confident will give you profits. Otherwise, why set aside an amount and invest every time?

2. Be disciplined enough to hold the stock

Dollar-cost averaging isn’t advisable for those who only want to invest for the short term. As it is a method of frequent investing, it follows that investors setting aside a sum to put into a stock at regular intervals would buy and hold the stock for years.

This, in itself, is quite difficult to stick with given the stock market volatility and its effects on investors’ emotions. But to succeed with this strategy, make sure you’re disciplined enough to consistently invest and wait for your gains.

Essentially, dollar-cost averaging makes investing a lot simpler. Still, this isn’t a recommendation to apply the same strategy. Remember your own goals in investing and assess whether DCA fits into your list.

Cheers! Hope to see you in our complimentary webinar that teaches all about stock investing. Don’t worry, it’s free for you because you’ve read this far!

Use this link to secure your FREE SEAT today.

DISCLAIMER

This article and its contents are provided for information purposes only and do not constitute a recommendation to purchase or sell securities of any of the companies or investments herein described. It is not intended to amount to financial advice on which you should rely.

No representations, warranties, or guarantees, whether expressed or implied, made to the contents in the article is accurate, complete, or up-to-date. Past performance is not indicative nor a guarantee of future returns.

We, 8VI Global Pte Ltd, disclaim any responsibility for any liability, loss, or risk or otherwise, which is incurred as a consequence, directly or indirectly, from the use and application of any of the contents of the article.